Marc Andreessen: From Midwestern Code to Silicon Valley Power Broker

Marc Lowell Andreessen stands as one of the defining figures of the digital age—a software engineer turned entrepreneur turned venture capitalist whose work has shaped how billions interact with the internet and how capital flows into the technologies of tomorrow. Born on July 9, 1971, in Cedar Falls, Iowa, and raised in the tiny rural town of New Lisbon, Wisconsin, Andreessen embodies the classic American tech success story: a self-taught programmer from modest Midwestern roots who moved to the Bay Area and helped ignite the internet revolution. His co-creation of the Mosaic web browser and co-founding of Netscape Communications in the early 1990s popularized the World Wide Web. Later, as co-founder of Andreessen Horowitz (a16z) in 2009, he reinvented venture capital itself.

Early Life and the University of Illinois: Seeds of InnovationAndreessen discovered computers young. By age 8 or 9, he taught himself BASIC programming from a library book on his family’s Commodore 64, writing games while his peers focused on football. School sports held little appeal for the tall, cerebral teen; coding did. In 1989, he enrolled at the University of Illinois at Urbana-Champaign (UIUC), drawn by its top computer science program and one of the nation’s four federally funded supercomputing centers—the National Center for Supercomputing Applications (NCSA). The campus was an early internet-native environment with high-speed connections rare elsewhere.

As an undergraduate, Andreessen landed a part-time job at NCSA. There, in 1992–1993, he collaborated with programmer Eric Bina to build Mosaic, the first widely used graphical web browser. Released in January 1993, Mosaic integrated images, point-and-click hyperlinks, and cross-platform usability—transforming the text-only, Unix-centric web into something accessible to everyday users. Over two million copies were downloaded in its first year, free from NCSA. It was a breakthrough that exploded the internet’s potential. Andreessen graduated with a BS in computer science in December 1993.

The Move from Illinois to the Bay Area: Chasing Startup GravityThe move from Illinois to California was not just geographic—it was cultural and career-defining. Andreessen has noted that the Midwest lacked startup infrastructure: “You just don’t start companies out there. The environment is all wrong. The culture is all wrong.” Champaign-Urbana offered world-class computing but no ecosystem for commercializing it. After graduation, he accepted a job at Enterprise Integration Technologies (EIT), a small Palo Alto firm focused on web security for e-commerce. He arrived in Silicon Valley in early 1994, rented a two-bedroom apartment, bought a Ford Mustang, and immersed himself in the Valley’s hardware-to-software shift.

Bored after three months at EIT, Andreessen connected with Jim Clark, founder of Silicon Graphics. Clark, seeking his next big idea, saw Mosaic’s potential. In April 1994, they founded Mosaic Communications Corporation in Mountain View—quickly renamed Netscape Communications after UIUC asserted rights to the “Mosaic” name. Andreessen recruited the original Mosaic team and became vice president of technology. The Bay Area provided venture funding, talent, and a risk-tolerant culture impossible in Illinois. Netscape Navigator launched commercially in late 1994, capturing over 75% browser market share by mid-1996 and accelerating the dot-com boom. Its 1995 IPO—valued at nearly $3 billion on its first day—symbolized the internet’s arrival.

Netscape’s success (later acquired by AOL) cemented Andreessen’s legend, but the move highlighted a broader truth: transformative tech requires the right ecosystem. Illinois gave him the technical foundation; the Bay Area supplied the oxygen for scaling it.Post-Netscape and the Birth of a16zAfter Netscape, Andreessen served briefly as AOL’s chief technology officer. He co-founded Loudcloud (later Opsware) with Ben Horowitz in 1999, a cloud services pioneer sold to HP for $1.6 billion in 2007. Horowitz had been Loudcloud’s CEO; their partnership proved enduring. By the late 2000s, both were “super angel” investors. In July 2009, they launched Andreessen Horowitz with a $300 million debut fund, betting that “software would eat the world” and that the biggest tech companies would dwarf prior valuations. The a16z Innovation: The Platform Venture Capital Modela16z’s core innovation was the “platform” model—treating venture capital like a full-service operating company rather than a small partnership dispensing checks and board seats. Traditional VC (pre-2009) relied on generalist partners providing capital, advice, and networks in a hands-off way. Funds were smaller; operational support was minimal. a16z built the largest team of operators in the industry: marketing, talent/recruiting, policy/legal, engineering, go-to-market, and finance experts who actively help portfolio companies scale. Investors are mostly ex-founders and operators organized by vertical (AI, crypto, bio, etc.). As of recent years, the firm employs over 500 people across specialized practices.

This “product-first” approach—building services for founders before they need them—flipped the script. Founders choose a16z not just for money but for systemic support that accelerates growth. It created a virtuous cycle: better support attracts top deal flow, which drives better returns, enabling larger funds. Post-a16z, the industry shifted. Many top firms adopted platform elements, but a16z scaled it first and largest, contributing to capital concentration among a few mega-firms. Companies now stay private longer and raise more capital; platforms help them navigate that. Why a16z Raises Such Big Money—and the Netscape Halo’s Rolea16z manages over $90 billion in assets under management as of early 2026, with massive recent raises (e.g., over $15 billion across funds in January 2026, representing ~18% of all U.S. VC dollars allocated in 2025). Large funds match exploding opportunity sizes in AI, infrastructure, bio, and “American Dynamism” (defense, supply chains). Companies require hundreds of millions (or billions) to scale before IPO; smaller funds can’t keep up. The platform model justifies scale—specialized teams manage complexity without diluting partner focus.

The Netscape halo undeniably helps. Andreessen’s status as an internet pioneer—co-creator of Mosaic, Netscape co-founder—gives instant credibility. Founders seek the “patron saint of the internet”; LPs trust the brand. This aura, amplified by bold public commentary and media savvy, draws elite deal flow and capital, sustaining the flywheel. a16z Track Record: Defining Wins in Techa16z’s portfolio exceeds 1,000 companies, with 35+ IPOs and 247+ acquisitions. Early funds delivered strong returns (Fund I ~6x). Major liquidity events peaked in 2021, contributing billions to LPs. The firm has backed 124+ unicorns, more than peers in recent periods.

Most successful companies (profiles):

Portfolio companies access networks, benchmarks, and hands-on help—e.g., GTM strategy, hiring at scale, regulatory navigation. This isn’t ad hoc advice; it’s institutionalized, proactive infrastructure. It lets startups move faster, hire better, and compete aggressively. The model also generates proprietary deal flow: top founders self-select for the full-stack partnership.

Legacy: Betting on Builders and the FutureFrom a Illinois dorm room to a16z’s Menlo Park headquarters, Marc Andreessen’s journey traces the internet’s maturation and venture capital’s professionalization. His Netscape move proved geography matters; a16z proved operational support can be venture’s unfair advantage. In an era of AI, biotech, and national competitiveness, a16z’s scale and platform position it to back the next wave—while its founder’s halo reminds us that one Midwestern kid with a browser can still reshape the world. The firm’s bet remains simple: the future belongs to builders, and a16z exists to give them every tool to win.

Marc Lowell Andreessen stands as one of the defining figures of the digital age—a software engineer turned entrepreneur turned venture capitalist whose work has shaped how billions interact with the internet and how capital flows into the technologies of tomorrow. Born on July 9, 1971, in Cedar Falls, Iowa, and raised in the tiny rural town of New Lisbon, Wisconsin, Andreessen embodies the classic American tech success story: a self-taught programmer from modest Midwestern roots who moved to the Bay Area and helped ignite the internet revolution. His co-creation of the Mosaic web browser and co-founding of Netscape Communications in the early 1990s popularized the World Wide Web. Later, as co-founder of Andreessen Horowitz (a16z) in 2009, he reinvented venture capital itself.

As an undergraduate, Andreessen landed a part-time job at NCSA. There, in 1992–1993, he collaborated with programmer Eric Bina to build Mosaic, the first widely used graphical web browser. Released in January 1993, Mosaic integrated images, point-and-click hyperlinks, and cross-platform usability—transforming the text-only, Unix-centric web into something accessible to everyday users. Over two million copies were downloaded in its first year, free from NCSA. It was a breakthrough that exploded the internet’s potential. Andreessen graduated with a BS in computer science in December 1993.

Bored after three months at EIT, Andreessen connected with Jim Clark, founder of Silicon Graphics. Clark, seeking his next big idea, saw Mosaic’s potential. In April 1994, they founded Mosaic Communications Corporation in Mountain View—quickly renamed Netscape Communications after UIUC asserted rights to the “Mosaic” name. Andreessen recruited the original Mosaic team and became vice president of technology. The Bay Area provided venture funding, talent, and a risk-tolerant culture impossible in Illinois. Netscape Navigator launched commercially in late 1994, capturing over 75% browser market share by mid-1996 and accelerating the dot-com boom. Its 1995 IPO—valued at nearly $3 billion on its first day—symbolized the internet’s arrival.

Netscape’s success (later acquired by AOL) cemented Andreessen’s legend, but the move highlighted a broader truth: transformative tech requires the right ecosystem. Illinois gave him the technical foundation; the Bay Area supplied the oxygen for scaling it.Post-Netscape and the Birth of a16zAfter Netscape, Andreessen served briefly as AOL’s chief technology officer. He co-founded Loudcloud (later Opsware) with Ben Horowitz in 1999, a cloud services pioneer sold to HP for $1.6 billion in 2007. Horowitz had been Loudcloud’s CEO; their partnership proved enduring. By the late 2000s, both were “super angel” investors. In July 2009, they launched Andreessen Horowitz with a $300 million debut fund, betting that “software would eat the world” and that the biggest tech companies would dwarf prior valuations. The a16z Innovation: The Platform Venture Capital Modela16z’s core innovation was the “platform” model—treating venture capital like a full-service operating company rather than a small partnership dispensing checks and board seats. Traditional VC (pre-2009) relied on generalist partners providing capital, advice, and networks in a hands-off way. Funds were smaller; operational support was minimal. a16z built the largest team of operators in the industry: marketing, talent/recruiting, policy/legal, engineering, go-to-market, and finance experts who actively help portfolio companies scale. Investors are mostly ex-founders and operators organized by vertical (AI, crypto, bio, etc.). As of recent years, the firm employs over 500 people across specialized practices.

This “product-first” approach—building services for founders before they need them—flipped the script. Founders choose a16z not just for money but for systemic support that accelerates growth. It created a virtuous cycle: better support attracts top deal flow, which drives better returns, enabling larger funds. Post-a16z, the industry shifted. Many top firms adopted platform elements, but a16z scaled it first and largest, contributing to capital concentration among a few mega-firms. Companies now stay private longer and raise more capital; platforms help them navigate that. Why a16z Raises Such Big Money—and the Netscape Halo’s Rolea16z manages over $90 billion in assets under management as of early 2026, with massive recent raises (e.g., over $15 billion across funds in January 2026, representing ~18% of all U.S. VC dollars allocated in 2025). Large funds match exploding opportunity sizes in AI, infrastructure, bio, and “American Dynamism” (defense, supply chains). Companies require hundreds of millions (or billions) to scale before IPO; smaller funds can’t keep up. The platform model justifies scale—specialized teams manage complexity without diluting partner focus.

The Netscape halo undeniably helps. Andreessen’s status as an internet pioneer—co-creator of Mosaic, Netscape co-founder—gives instant credibility. Founders seek the “patron saint of the internet”; LPs trust the brand. This aura, amplified by bold public commentary and media savvy, draws elite deal flow and capital, sustaining the flywheel. a16z Track Record: Defining Wins in Techa16z’s portfolio exceeds 1,000 companies, with 35+ IPOs and 247+ acquisitions. Early funds delivered strong returns (Fund I ~6x). Major liquidity events peaked in 2021, contributing billions to LPs. The firm has backed 124+ unicorns, more than peers in recent periods.

Most successful companies (profiles):

- Airbnb (Series B, 2011): a16z partner Jeff Jordan led investment, spotting two-sided marketplace dynamics amid regulatory skepticism. IPO in 2020 valued it at ~$47 billion initially (now far higher in market cap). Transformed travel and short-term rentals.

- Coinbase (Series B, 2013): Marc Andreessen championed Bitcoin as a computer-science breakthrough. Early bet on crypto infrastructure; IPO in 2021 reached ~$86 billion valuation. Pioneered mainstream crypto adoption.

- Slack (Series A, 2014): Partner Chris Dixon saw workplace collaboration revolution. Acquired by Salesforce for $27.7 billion in 2020. Redefined team communication.

- GitHub (2012 investment): $100 million bet on open-source platform; acquired by Microsoft for $7.5 billion (a16z returned over $1 billion). Catalyzed developer tools ecosystem.

- Brian Chesky (Airbnb co-founder/CEO): Former designer who scaled a marketplace into a global hospitality giant. a16z’s support helped navigate growth and regulation. Chesky’s focus on community and experience aligns with platform thinking.

- Brian Armstrong (Coinbase co-founder/CEO): Visionary who built crypto on-ramp for millions. Andreessen’s early endorsement and a16z’s operational help fueled compliance and expansion amid volatility. Armstrong’s long-term crypto conviction mirrors the firm’s thesis.

- Stewart Butterfield (Slack co-founder/CEO): Pivoted a gaming company’s internal tool into enterprise software. Dixon’s investment and a16z platform aided rapid scaling and acquisition. Butterfield’s product intuition exemplifies the founder-operators a16z attracts.

Portfolio companies access networks, benchmarks, and hands-on help—e.g., GTM strategy, hiring at scale, regulatory navigation. This isn’t ad hoc advice; it’s institutionalized, proactive infrastructure. It lets startups move faster, hire better, and compete aggressively. The model also generates proprietary deal flow: top founders self-select for the full-stack partnership.

The Venture Capital Renaissance: Parallel Tech Explosions and the New North Star for Investors

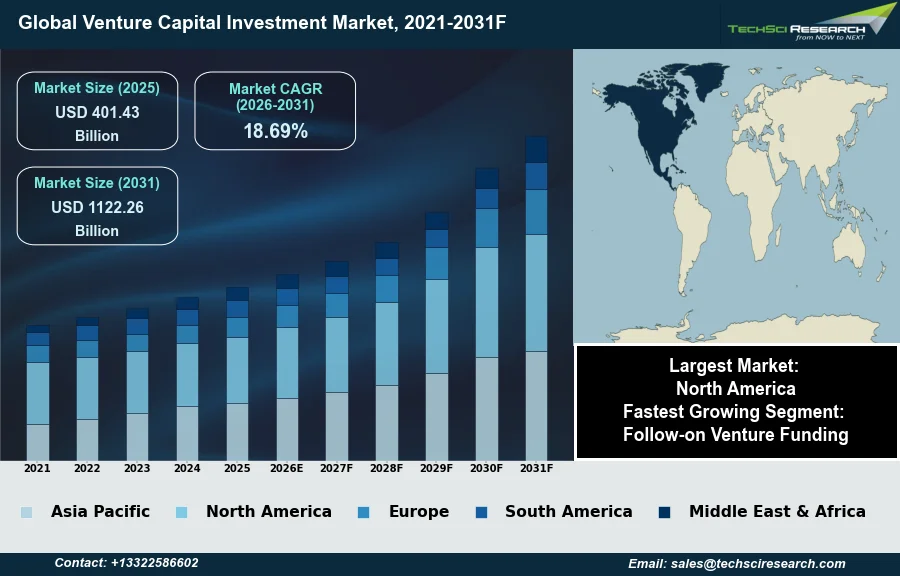

Venture capital (VC) in 2026 stands at an inflection point of historic scale and complexity. Global startup funding reached approximately $425 billion in 2025—the third-highest year on record—up 30% from 2024, with the U.S. capturing a dominant 64% share at ~$274 billion (and $340 billion in some estimates). Early 2026 data shows continued momentum, with Q1 deal value already shattering records. Yet beneath the headline numbers lies a profound shift: innovation is not merely accelerating—it is exploding across at least a dozen internet-scale technologies simultaneously, each with the disruptive potential of the original web or mobile eras. These waves intersect in ways that create both unprecedented opportunity and existential chaos for investors.

The correct response is not to chase every shiny new technology. It is to ignore the tech itself as the primary signal and instead fixate on the entrepreneurs tackling humanity’s biggest, most intractable problems—climate collapse, energy abundance, healthspan extension, national security, and equitable access to opportunity. That problem-first orientation is the only reliable north star in this maelstrom.Silicon Valley: Still the Undisputed Capital of Risk CapitalSilicon Valley remains the gravitational center of global VC, commanding roughly 40% of all U.S. Seed and Series A capital—more than New York, Boston, and Los Angeles combined. In 2025, the Bay Area’s ecosystem powered the AI mega-deal surge that drove national totals to their second-strongest year ever. Platform firms like Andreessen Horowitz, Sequoia, and Kleiner Perkins continue to dominate, but the region’s edge now extends beyond software into “hard tech”: AI infrastructure, robotics, energy systems, and defense.

The Valley’s strength is its density—talent, capital, and ambition in one place—but its risk is echo-chamber concentration. AI captured 65% of U.S. VC deal value in 2025, creating a winner-take-most dynamic that leaves many non-AI founders starved for attention. The Broader U.S.: Decentralizing Innovation HubsWhile Silicon Valley leads, capital is diffusing. Austin, Miami, New York, Boston, and emerging “American Dynamism” clusters (defense, manufacturing, supply chains) are capturing meaningful share. North America as a whole accounted for 46% of the global VC market in 2025, with early-stage resilience and late-stage mega-rounds returning. Defense tech funding alone jumped 75% year-over-year into 2025. The U.S. retains unmatched depth in university spinouts, corporate venture arms, and exit pathways (IPOs and M&A both rebounded sharply). India: Disciplined Growth Amid Global HeadwindsIndia’s VC/growth equity market hit ~$16 billion in 2025 (up ~1.2x from 2024), marking the second straight year of expansion while broader private capital slowed. Total PE/VC reached $60.7 billion across 1,475 deals—the highest deal count ever. Fundraising nearly doubled to $5.4 billion for VC/growth funds, with larger vehicles ($100M+) driving the surge. Sectors shifting toward AI, deeptech, SaaS, fintech, climate, space, and industrial tech. Exits improved, and the ecosystem matured toward sustainability over pure scale. India is now Asia-Pacific’s second-largest VC destination after China, powered by domestic consumption, regulatory tailwinds, and digital infrastructure. China: State-Led Hard-Tech RenaissanceChina’s VC ecosystem is undergoing a deliberate pivot from consumer internet to “new quality productive forces”—semiconductors, quantum, biotech, brain-computer interfaces, robotics, and aerospace. In late 2025, Beijing launched a national venture capital guidance fund (part of three state-backed vehicles totaling over $21 billion) explicitly targeting these hard technologies. Early 2026 fundraising hit record quarterly pace, with government and corporate capital dominating large deals. While overall private VC remains smaller than the U.S., China captured ~5% of global AI VC in 2025 and leads in applied robotics and manufacturing scale. Regulatory easing on cross-border M&A and IPOs signals renewed liquidity focus.

Global VC: Europe, Israel, and Emerging Markets RisingEurope is maturing with deep-science plays (quantum, biotech, climate). Israel remains a defense and cybersecurity powerhouse. Latin America, Africa, and the Middle East show explosive fintech and stablecoin growth, with liquidity events accelerating. Southeast Asia and the Middle East are drawing cross-border capital. Overall, global VC is diversifying geographically even as capital concentrates thematically. The Explosion: At Least 10 Internet-Scale Technologies Advancing in ParallelInnovation velocity has entered a new regime. Where the 1990s saw one transformative wave (the commercial internet) and the 2010s another (mobile + cloud), 2026 features a minimum of ten parallel, self-reinforcing megatrends—each capable of creating trillion-dollar markets on its own:

The Core VC Challenge: Chaos in the Tech MaelstromThis parallel explosion is the single greatest challenge facing venture capital today. Traditional VC operated in relatively linear waves: spot the next platform shift, back the best teams executing it. Today, capital, talent, and founder attention are fragmented across dozens of frontier domains. Mega-deals concentrate in a handful of AI winners, while thousands of equally promising deep-tech or climate plays starve. LPs demand returns in compressed timeframes, yet many of these technologies require patient, decade-long capital. The risk of distraction is acute—investors can easily chase hype cycles and miss the intersections that create enduring value.The North Star Thesis: Forget the Technology—Bet on Entrepreneurs Solving the Biggest ProblemsIn this environment, the winning strategy is brutally simple: ignore the specific technology du jour. Obsess over founders who are maniacally focused on solving the largest, most painful problems facing humanity and civilization. Climate resilience, affordable energy, scalable healthcare, secure supply chains, defense superiority—these are not “sectors.” They are existential mandates that will inevitably pull in whatever combination of the exploding technologies is required.

Problem-first founders possess the clarity to navigate chaos. They treat AI, quantum, biotech, and robotics as tools in a toolbox, not the mission itself. They build antifragile companies that compound across waves rather than riding any single one. History proves the pattern: the greatest fortunes were made by those who solved real pain at scale (Amazon: commerce infrastructure; Google: information access; Tesla/SpaceX:

energy and multiplanetary survival). In 2026 and beyond, the same logic holds at hyper-speed.

The Path ForwardVenture capital’s role has never been more vital—or more demanding. The industry must evolve toward deeper specialization within verticals while maintaining cross-domain fluency. Platforms that provide operational support across multiple technologies (talent, policy, go-to-market) will thrive. Global diversification will hedge regional risks. But above all, the timeless truth endures: technology is transient; world-class entrepreneurs who fix what’s broken are eternal.

The parallel explosions are not a bug—they are the feature. The VCs who thrive will be those who stop worshipping the tools and start backing the builders who wield them to solve humanity’s greatest challenges. That is the only north star capable of guiding capital through the beautiful, overwhelming chaos of 2026 and the decade ahead.

Venture capital (VC) in 2026 stands at an inflection point of historic scale and complexity. Global startup funding reached approximately $425 billion in 2025—the third-highest year on record—up 30% from 2024, with the U.S. capturing a dominant 64% share at ~$274 billion (and $340 billion in some estimates). Early 2026 data shows continued momentum, with Q1 deal value already shattering records. Yet beneath the headline numbers lies a profound shift: innovation is not merely accelerating—it is exploding across at least a dozen internet-scale technologies simultaneously, each with the disruptive potential of the original web or mobile eras. These waves intersect in ways that create both unprecedented opportunity and existential chaos for investors.

The correct response is not to chase every shiny new technology. It is to ignore the tech itself as the primary signal and instead fixate on the entrepreneurs tackling humanity’s biggest, most intractable problems—climate collapse, energy abundance, healthspan extension, national security, and equitable access to opportunity. That problem-first orientation is the only reliable north star in this maelstrom.Silicon Valley: Still the Undisputed Capital of Risk CapitalSilicon Valley remains the gravitational center of global VC, commanding roughly 40% of all U.S. Seed and Series A capital—more than New York, Boston, and Los Angeles combined. In 2025, the Bay Area’s ecosystem powered the AI mega-deal surge that drove national totals to their second-strongest year ever. Platform firms like Andreessen Horowitz, Sequoia, and Kleiner Perkins continue to dominate, but the region’s edge now extends beyond software into “hard tech”: AI infrastructure, robotics, energy systems, and defense.

The Valley’s strength is its density—talent, capital, and ambition in one place—but its risk is echo-chamber concentration. AI captured 65% of U.S. VC deal value in 2025, creating a winner-take-most dynamic that leaves many non-AI founders starved for attention. The Broader U.S.: Decentralizing Innovation HubsWhile Silicon Valley leads, capital is diffusing. Austin, Miami, New York, Boston, and emerging “American Dynamism” clusters (defense, manufacturing, supply chains) are capturing meaningful share. North America as a whole accounted for 46% of the global VC market in 2025, with early-stage resilience and late-stage mega-rounds returning. Defense tech funding alone jumped 75% year-over-year into 2025. The U.S. retains unmatched depth in university spinouts, corporate venture arms, and exit pathways (IPOs and M&A both rebounded sharply). India: Disciplined Growth Amid Global HeadwindsIndia’s VC/growth equity market hit ~$16 billion in 2025 (up ~1.2x from 2024), marking the second straight year of expansion while broader private capital slowed. Total PE/VC reached $60.7 billion across 1,475 deals—the highest deal count ever. Fundraising nearly doubled to $5.4 billion for VC/growth funds, with larger vehicles ($100M+) driving the surge. Sectors shifting toward AI, deeptech, SaaS, fintech, climate, space, and industrial tech. Exits improved, and the ecosystem matured toward sustainability over pure scale. India is now Asia-Pacific’s second-largest VC destination after China, powered by domestic consumption, regulatory tailwinds, and digital infrastructure. China: State-Led Hard-Tech RenaissanceChina’s VC ecosystem is undergoing a deliberate pivot from consumer internet to “new quality productive forces”—semiconductors, quantum, biotech, brain-computer interfaces, robotics, and aerospace. In late 2025, Beijing launched a national venture capital guidance fund (part of three state-backed vehicles totaling over $21 billion) explicitly targeting these hard technologies. Early 2026 fundraising hit record quarterly pace, with government and corporate capital dominating large deals. While overall private VC remains smaller than the U.S., China captured ~5% of global AI VC in 2025 and leads in applied robotics and manufacturing scale. Regulatory easing on cross-border M&A and IPOs signals renewed liquidity focus.

- Artificial Intelligence / Agentic & Physical AI — From generative models to autonomous agents and humanoid robotics.

- Biotechnology & Synthetic Biology — CRISPR successors, mRNA platforms, xenotransplantation, longevity therapeutics.

- Quantum Computing — Error-corrected systems poised for optimization, simulation, and cryptography breakthroughs.

- Robotics & Embodied AI — Humanoids, drones, and factory-scale automation eliminating labor bottlenecks.

- Climate Tech & Energy Abundance — Advanced nuclear, next-gen batteries, carbon capture, fusion pilots.

- Commercial Space & Orbital Infrastructure — Reusable rockets, satellite mega-constellations, space manufacturing.

- Brain-Computer Interfaces & Neurotech — Direct mind-machine links for medicine, augmentation, and computing.

- Advanced Materials & Semiconductors — Photonics, 2D materials, neuromorphic chips beyond Moore’s Law.

- Cybersecurity & Cryptography — Post-quantum encryption, AI-driven threat detection, decentralized security.

- Defense Tech / Dual-Use Systems — Autonomous weapons, hypersonics, resilient supply chains (“American Dynamism”).

- Autonomous Mobility & Infrastructure — Self-driving at scale, drone delivery, smart cities.

Problem-first founders possess the clarity to navigate chaos. They treat AI, quantum, biotech, and robotics as tools in a toolbox, not the mission itself. They build antifragile companies that compound across waves rather than riding any single one. History proves the pattern: the greatest fortunes were made by those who solved real pain at scale (Amazon: commerce infrastructure; Google: information access; Tesla/SpaceX:

energy and multiplanetary survival). In 2026 and beyond, the same logic holds at hyper-speed.

The parallel explosions are not a bug—they are the feature. The VCs who thrive will be those who stop worshipping the tools and start backing the builders who wield them to solve humanity’s greatest challenges. That is the only north star capable of guiding capital through the beautiful, overwhelming chaos of 2026 and the decade ahead.

No comments:

Post a Comment